Four.meme: How to Turn the BSC Chain into a DeFi Meme Wonderland Using AI Concept

Original Title: "How Four.meme Turned BSC Chain into a Leek Magic Experimental Field with AI Concepts"

Original Author: Lawrence, Mars Finance

Foreword: An Art Performance That Can't Even Bother with "Surface Kung Fu"

Old leeks who have been in the crypto circle for many years are already accustomed to the classic three-piece suit used by project teams: drawing pies with PPT, spinning stories with a whitepaper, and giving buy signals through KOLs.

However, in the early morning of April 18, 2025, during the SKYAI presale project launched by the Four.meme platform, the posture of "writing perfunctorily on the face and engraving the harvest leek into DNA" refreshed the industry's lower limit. This magical drama, which combines "AI concept bombing," "rule black hole," "contract address typos," and "CZ's mystical retweet," can be described as the blockchain version of "The Emperor's New Clothes"—the project team parading naked, while the onlookers insist on praising the clothes as beautiful.

This article will dissect the new clothes of SKYAI from four dimensions: "technology hollowing," "rule opacity," "platform disqualification," and "community madness," and explore how Four.meme has fallen from a "Meme Launchpad" to a "Leek Shredder."

Chapter 1 Technology Section: When the "AI Protocol" Falls into the "Emperor's New Code"

1.1 MCP Protocol? Better Rename It to "Make Crypto Pretend"

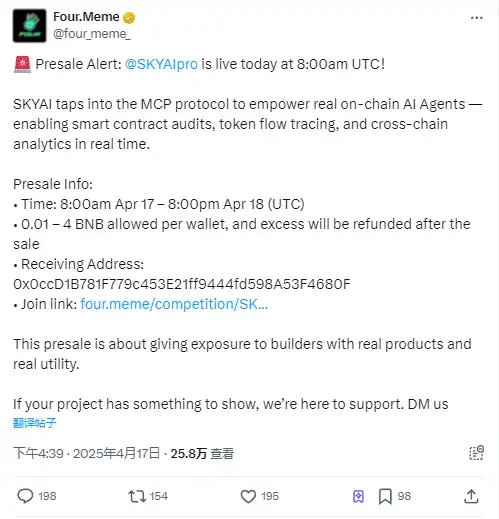

SKYAI claims that its core is the MCP protocol (Machine-Contract Protocol), which is said to enable AI to achieve "smart contract audits," "cross-chain data tracking," and "real-time on-chain analysis." However, looking at the project's information, it's full of Internet jargon like "empowerment," "upgrade," "next generation," with specific technical details more mysterious than Satoshi Nakamoto's true identity. This is reminiscent of the classic tactic in e-commerce presales where "consumer is deceived with model photos, while actual delivery is flea market goods."

Even more absurdly, the project team forcefully "collided" OpenAI's Function Calling and Anthropic's Claude model, claiming to "integrate local tools into the BSC chain." However, upon closer inspection, the so-called "technical breakthrough" is nothing more than renaming the API interface of ChatGPT—similar to packaging "45-day presale delivery" as "artisan spirit slow living."

1.2 Roadmap: ETH/Base Chain Support? Why Not Just Say "Schrodinger's Multi-chain"?

SKYAI's roadmap is like a page from an e-commerce platform that "does not indicate shipping time on the pre-order page, only reveals it after payment, stating a one-month wait."

Despite primarily focusing on the BSC chain, mentioning ETH/Base support in the plan is akin to a restaurant selling "freshly stir-fried crayfish," then informing customers, "The crayfish are still growing in the lake; pay first, and it will be served in three years." This "harvesting current funds with future concepts" tactic is so audacious that even the Jiangsu Provincial Consumer Protection Commission would acknowledge its expertise.

Chapter 2 Rulebook: It's Not about Being Darker; It's about a Darker "Rug Pull Playbook"

2.1 No Presale Cap: Contemporary "Ponzi Scheme" Art Performance

SKYAI's presale rules can be considered the crypto version of a "Rule of the Ruthless": no upper limit on the amount, no token distribution details, and rules revealed only after it ends. This is like an online seller saying, "Dear, pay first, and we'll tell you what you bought when it arrives." With reference to the China Consumers Association's characterization of "ultra-long presales," this operation is suspected of leveraging its dominant position to shift risks onto investors—essentially engaging in "bullying through standard contract" towards investors.

2.2 Incorrect Contract Address: Not Even Bothering to Pretend to Be "Professional Fumbling"

If the project team can mistakenly type the CA address, it's akin to an e-commerce merchant "mistakenly listing a link for a down jacket as a short-sleeved shirt."

What's even more surreal is that some community members argue, "This is an anti-whale strategy!"—Following this logic, a bank's ATM dispensing counterfeit money could also be explained as an "anti-money laundering innovation." This kind of "packaging accidents as stories" rhetoric would even make Pinduoduo's "Slash the Price" algorithm bow in defeat.

Chapter 3 Platform Play: How Four.meme Shifted from a "Launchpad" to a "Rug Pull Incinerator"

3.1 Launch Platform Hosting IDOs? How about Switching to Selling "Air Coin Blind Boxes"?

As a Meme coin launchpad, Four.meme should have been the guardian of a "fair launch" but instead personally partook in promoting presales, akin to a Taobao customer service representative opening a store to sell counterfeit goods. Its actions completely contradict the decentralization spirit of Web3 and instead replicate the monopoly tactics of e-commerce platforms, playing both the judge and the player. Considering Four.meme's past of being hacked for $15,000 due to a contract flaw, endorsing SKYAI this time is more like a gambler's "desperate move in a crisis."

3.2 CZ Retweet Metaphysics: Modern "Shitcoin" Behavioral Economics

The community has developed a bizarre consensus that "CZ loves to retweet shit, just go all in," essentially alienating investment into a "retweet lottery."

Similar to the consumer psychology of "knowing it's a scam but still betting on the seller to deliver" in e-commerce pre-sales, rug pull victims have long been trapped in the "sunk cost fallacy delusion": since the BSC chain is the "chain of beasts," it's better to voluntarily become "feed" — this kind of magical realism is something even Marquez novels dare not write about.

Chapter 4 Ecology: Why BSC Chain Has Become a "Magical Realism Test Field"

4.1 From "Innovation Hub" to "Scam Breeding Ground": A Brief History of the BSC Chain's Downfall

Four.meme claimed that its four projects were selected for the BNB Chain's $100 million incentive plan, but the SKYAI incident exposed a deep crisis in the BSC ecosystem: heavy on marketing, light on technology; heavy on traffic, light on compliance; heavy on hype, light on value. This closely resembles the logic of e-commerce platforms that tolerate "super long pre-sales" — pleasing the capital market with GMV data at the expense of consumer trust. The characterization of "unfair clauses" by the Jiangsu Consumer Protection Commission seems perfectly fitting in the context of the BSC chain.

4.2 The Birth of the "Chain of Beasts": When Everyone Is Pretending to Play Games

The community's nickname for the BSC chain, the "chain of beasts," is essentially a collective catharsis of systemic disorder. Just as e-commerce platforms turn a blind eye to merchants "reselling returned goods," Four.meme's tolerance of SKYAI reflects the entire ecosystem's "race to the bottom": whoever can harvest rug pull victims faster is the "innovation pioneer." This distorted set of values has allowed blockchain technology to be completely reduced to a tool for "Ponzi magic."

Conclusion: Maintaining Sobriety in the "Clown Era" in N Ways

The SKYAI pre-sale farce is essentially a microcosm of the cryptocurrency world's "bad money drives out good money" scenario. When the technological narrative becomes a tool for rug pulls, community consensus devolves into retweet metaphysics, and platform credibility loses to traffic anxiety.

For the average investor, the author's advice is only threefold:

· Stay Away from "Three-No Pre-Sales": Projects with no technical whitepaper, no on-chain audit, and no clear rules are essentially P2P scams masquerading in Web3 clothing.

· Beware of "KOL Pyramid Schemes": Treating CZ's retweets as investment advice is akin to buying financial products based on Li Jiaqi's livestreams — the former may make you lose money, while the latter will at least get you a face mask.

· Understand the Nature of the Platform: When Four.meme started selling "Air Coin Blind Boxes," its business model had fallen from a "service fee model" to a "scam profit-sharing model."

You can temporarily deceive all the rug pull victims, or you can deceive some rug pull victims forever, but you cannot deceive all rug pull victims forever—unless the rug pull victims choose to play dead voluntarily.

You may also like

$75 billion in foreign capital has fled, and South Korean retail investors have absorbed it all using leverage

Bitcoin Trading Guide 2026: Strategies for Experienced Traders

What Is XAUT and PAXG? Why Tokenized Gold Is Booming in 2026

Cryptocurrency CEXs are flocking to sell US stocks, and traditional brokerages are facing an "uninvited guest."

Will the SpaceX IPO Hurt Bitcoin? Here's What Traders Are Watching

Foreign selling in the South Korean stock market accelerates, with cumulative net sales reportedly reaching $75 billion this year

On June 9, The Kobeissi Letter, citing Goldman Sachs data, reported that global investors are selling South Korean stocks at an unusually rapid pace. In the latest trading session, foreign investors sold about $801 million worth of Kospi constituent stocks again; total foreign outflows last week reached about $10 billion, and the market has been in net foreign selling on nearly every trading day over the past month. According to the data cited in the report, foreign investors have sold about $75 billion worth of South Korean stocks so far this year. Meanwhile, South Korean retail and institutional investors together recorded roughly $69 billion in net buying over the same period, suggesting that the market’s main buying support has come from domestic capital rather than returning overseas funds. The information currently disclosed still mainly comes from The Kobeissi Letter’s retelling and Goldman Sachs data summaries, while public details on the statistical period and the specific definition of “selling” remain relatively limited.

Fortune Warns of Strategy’s Financing Structure Risks as Bitcoin Premium Narrows

Fortune warned that Strategy’s Bitcoin treasury model faces growing financing risks as MSTR’s net asset premium narrows and preferred stock dividend pressure increases.

Ferrari Challenge Le Mans: Carl Moon to Dominate in WEEX Livery

Sahara AI Responds to SAHARA’s Sharp Drop: No Contract or Product Security Issues Found, Internal Investigation Underway

Sahara AI responded to SAHARA’s 60% price drop, saying no token contract or product security issues have been found and an internal investigation is underway.

WEEX Deposit/Withdrawal Dynamic Island: Your Asset Status, Always in Sight

Scaling Crypto Derivatives: The Digital Asset Infrastructure Behind High-Volume Trading

In the fast-moving digital asset ecosystem, derivatives platforms face an extreme architectural test. High-leverage futures markets demand more than just standard security—they require absolute operational precision, zero-latency matching engines, and ironclad structural scalability, all while navigating intense market volatility.

As global platforms scale to meet these demands, the industry is shifting away from rigid, monolithic setups toward a more agile, "decoupled" infrastructure philosophy.

The Blueprint for High-Volume Copy TradingFor elite global exchanges like WEEX (founded in 2018), this architectural choice becomes critical when scaling high-volume retail features like social copy trading. When thousands of users automatically mirror the real-time strategies of elite traders simultaneously, it triggers sudden, monumental spikes in concurrent transactional volume.

To prevent execution latency or settlement bottlenecks during these peak volatility events, a platform's primary engine must remain entirely dedicated to risk management, copy-trade synchronization, and order matching.

The Architectural Rule: New-generation platforms must separate front-end user execution engines from heavy backend infrastructural overhead to eliminate operational friction.

By separating these layers, platforms can maintain complete sovereignty over their trading environments and user experiences while strategically aligning with institutional-grade infrastructure ecosystems. This strategic framework allows modern exchanges to leverage advanced Digital Asset Custody infrastructure such as Cobo’s behind the scenes, ensuring that backend wallet management scales elastically alongside trading spikes.

Capitalizing on Market Momentum and 400× LeverageIn a derivatives arena where platforms offer up to 400× leverage on perpetual contracts, capital efficiency and market agility are core business metrics. To capture market momentum, an exchange needs the ability to rapidly expand its asset offerings, supporting everything from legacy crypto assets to sudden, trending altcoins across a massive library of trading pairs.

Adopting a flexible, scalable Wallet-as-a-Service (WaaS) solution such as Cobo’s could completely rewrite the development timeline for high-growth exchanges. Instead of spending months of engineering capital building out custom backend wallet architectures for every new blockchain network, platforms can deploy localized infrastructure in days.

This agility allows platforms to instantly scale their listings to over a thousand trading pairs without compromising security or delaying time-to-market. It mirrors the exact operational advantages seen during high-velocity market events, similar to how advanced wallet infrastructure empowers platforms during sudden asset surges; allowing exchanges to pass that speed and liquidity directly to their global user base.

A Mature Foundation for GrowthThe synergy between trusted infrastructure ecosystems and global trading platforms represents the natural evolution of a maturing crypto market. As WEEX continues to scale its global spot and derivatives offerings for over 6 million users, adopting robust backend paradigms proves that platforms no longer have to compromise between cutting-edge trading velocity and uncompromised structural security.

Morning Report | BitMine increased its holdings by 126,971 ETH last week; trader Eugene announced his exit from the crypto market

Wang Chuan: How can one not feel anxious after the neighbor Old Wang made thirty times profit by investing in storage stocks? (Seven) - A quarter-century cycle

Get Paid to Onboard? Try WEEX’s New Homepage with Rewards for Registration, Deposit & Trade

WEEX Custom Layout: Build Your Perfect Trading Workspace in Seconds

See “Buy Walls” & “Sell Walls” Instantly: WEEX Launches the Depth Chart for Smarter Trades

What Is Quick Trade on WEEX? 2 Ways WEEX Ends Chart-Panel Jumping

Morning News | Five major virtual asset platforms in South Korea have experienced 57 incidents of hacking and system failures in six years; Grayscale submits registration application for Canton ETF

$75 billion in foreign capital has fled, and South Korean retail investors have absorbed it all using leverage

Bitcoin Trading Guide 2026: Strategies for Experienced Traders

What Is XAUT and PAXG? Why Tokenized Gold Is Booming in 2026

Cryptocurrency CEXs are flocking to sell US stocks, and traditional brokerages are facing an "uninvited guest."

Will the SpaceX IPO Hurt Bitcoin? Here's What Traders Are Watching

Foreign selling in the South Korean stock market accelerates, with cumulative net sales reportedly reaching $75 billion this year

On June 9, The Kobeissi Letter, citing Goldman Sachs data, reported that global investors are selling South Korean stocks at an unusually rapid pace. In the latest trading session, foreign investors sold about $801 million worth of Kospi constituent stocks again; total foreign outflows last week reached about $10 billion, and the market has been in net foreign selling on nearly every trading day over the past month. According to the data cited in the report, foreign investors have sold about $75 billion worth of South Korean stocks so far this year. Meanwhile, South Korean retail and institutional investors together recorded roughly $69 billion in net buying over the same period, suggesting that the market’s main buying support has come from domestic capital rather than returning overseas funds. The information currently disclosed still mainly comes from The Kobeissi Letter’s retelling and Goldman Sachs data summaries, while public details on the statistical period and the specific definition of “selling” remain relatively limited.