Vitalik's Long-Term L1 Execution Layer Proposal Full Text: Replacing EVM with RISC-V

Original Title: Long-term L1 execution layer proposal: replace the EVM with RISC-V

Original Source: Vitalik Buterin

Original Translation: KarenZ, Foresight News

On April 20, Vitalik Buterin proposed a significant proposal regarding Ethereum's long-term L1 execution layer on the Ethereum Magicians platform. He suggested adopting the RISC-V architecture to replace the existing EVM (Ethereum Virtual Machine) as the virtual machine language for writing smart contracts. The goal is to fundamentally improve the efficiency of the Ethereum execution layer, overcome one of the current major scalability bottlenecks, and greatly simplify the elegance of the execution layer.

Foresight News has provided a full translation of the proposal to help readers understand this technological vision. The following is the translated content of the original proposal:

This article presents a radical idea about the future of the Ethereum execution layer, with ambitions no less than the Beam Chain plan for the consensus layer. The proposal aims to significantly enhance the efficiency of the Ethereum execution layer, address a major scalability bottleneck, and substantially simplify the execution layer—indeed, this may be the only way to achieve this goal.

Core Concept: Replace the EVM with RISC-V as the virtual machine language for smart contract writing.

Important Notes:

· Concepts such as account system, cross-contract calls, storage, etc., will be fully retained. These abstract designs work well, and developers are already accustomed to using them. Opcodes like SLOAD, SSTORE, BALANCE, CALL will be transformed into RISC-V system calls.

· In this mode, smart contracts can be written in Rust, but I expect most developers will continue to use Solidity (or Vyper) to write contracts, and these languages will be adapted to RISC-V as the new backend. Because smart contracts written in Rust are actually less readable, while Solidity and Vyper are clearer and more readable. The development experience may be hardly affected, and developers may not even notice the change.

· Old version EVM contracts will continue to operate and will be fully interoperable with new RISC-V contracts. There are several ways to achieve this, which will be discussed in detail later in this article.

The Nervos CKB VM has set a precedent as it is essentially an implementation of RISC-V.

Why is this done?

In the short term, upcoming EIPs (such as Block Access Lists, Delayed Execution, Distributed History Store, and EIP-4444) will address Ethereum's L1 main scalability bottlenecks. In the medium term, more issues will be addressed through statelessness and ZK-EVM. In the long term, the main limiting factors for Ethereum L1 scalability will be:

1. The stability of data availability sampling and historical storage protocols

2. The need to maintain block production market competitiveness

3. The proof capability of ZK-EVM

I will argue that replacing ZK-EVM with RISC-V can address key bottlenecks in (2) and (3).

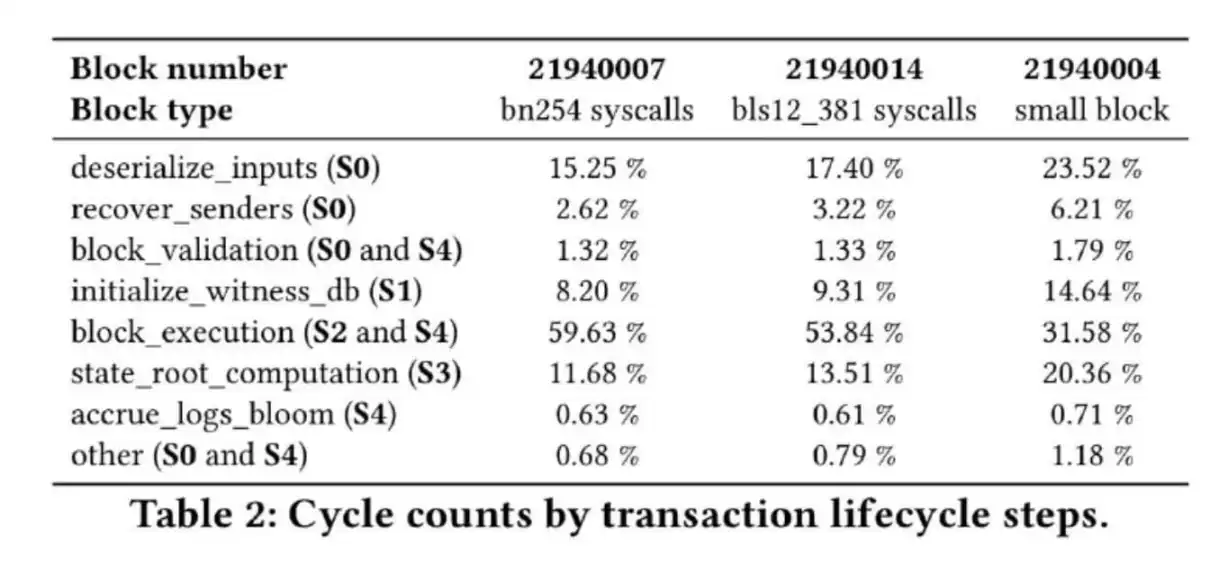

The table below shows the number of cycles required at each step of Succinct ZK-EVM proof of EVM execution layer:

Chart Description: The four main time-consuming steps are deserialize_inputs, initialize_witness_db, state_root_computation, and block_execution

Where initialize_witness_db and state_root_computation are related to the state tree, deserialize_inputs involves the process of converting block and witness data into an internal representation—actually more than 50% proportional to the witness size.

By replacing the current keccak 16-ary Merkle Patricia Tree with a binary tree that uses hash functions easy to prove, these parts can be significantly optimized. If Poseidon is used, we can prove 2 million hash values per second on a laptop (compared to approximately 15,000 hash/sec for keccak). Besides Poseidon, there are many other options. Overall, these components have a lot of optimization potential. Additionally, we can eliminate accrue_logs_bloom by removing bloom.

The remaining block_execution accounts for about half of the current proof cycle. To achieve a 100x overall proof efficiency improvement, the EVM proof efficiency needs to be improved at least 50 times. One solution is to create a more efficient proof implementation for EVM, and another is to note that the current ZK-EVM prover actually proves the EVM by compiling it into RISC-V, allowing smart contract developers direct access to this RISC-V virtual machine.

Some data indicates that in specific scenarios, efficiency gains of over 100x are possible:

In practical applications, the remaining prover time may be predominantly taken up by the current precompiles operation. If RISC-V is used as the main virtual machine, the Gas schedule will reflect actual proving time, and economic pressures will prompt developers to reduce the use of high-cost precompiles. Even so, the gains will not be as significant, but we have good reason to believe that these gains will be substantial.

(It is worth noting that in a typical EVM execution, the time spent on "EVM operations" versus "other operations" is also close to 50/50, so we intuitively believe that removing the EVM as an "intermediate layer" will bring equally significant gains.)

Implementation Details

There are various ways to implement this proposal. The least disruptive approach is to support both virtual machines simultaneously, allowing contracts to choose one to write. Both types of contracts will have access to the same functionality: persistent storage (SLOAD/SSTORE), the ability to hold an ETH balance, initiate/receive calls, etc. EVM and RISC-V contracts can call each other— from the RISC-V perspective, calling an EVM contract is akin to performing a system call with special parameters; and an EVM contract receiving a message will interpret it as a CALL.

From a protocol perspective, a more aggressive approach is to convert existing EVM contracts into calls to an EVM interpreter contract written in RISC-V, running its existing EVM code. That is, if an EVM contract has code C, and the EVM interpreter is at address X, the contract will be replaced with top-level logic that, when called with external parameters D, calls X and passes (C, D), then waits for a return value and forwards it. If the EVM interpreter itself calls the contract, requesting to perform CALL or SLOAD/SSTORE, the contract carries out these operations.

A compromise approach is to adopt the second approach but explicitly support the concept of a "virtual machine interpreter" in the protocol, requiring its logic to be written in RISC-V. EVM will be the initial instance, with potential future support for other languages (Move may be a candidate).

The core advantage of the second and third approaches are that they can greatly simplify the execution layer specification. Considering that even the incremental simplification of removing SELFDESTRUCT is fraught with difficulties, this approach may be the only feasible path to simplification. Tinygrad adheres to the strict rule of "code not exceeding 10,000 lines," and the optimal blockchain base layer should easily meet this limit, further streamlining the process. The Beam Chain project is expected to significantly simplify the Ethereum consensus layer, and for the execution layer to achieve similar improvements, this radical change may be the only viable path forward.

You may also like

$75 billion in foreign capital has fled, and South Korean retail investors have absorbed it all using leverage

Bitcoin Trading Guide 2026: Strategies for Experienced Traders

What Is XAUT and PAXG? Why Tokenized Gold Is Booming in 2026

Cryptocurrency CEXs are flocking to sell US stocks, and traditional brokerages are facing an "uninvited guest."

Will the SpaceX IPO Hurt Bitcoin? Here's What Traders Are Watching

Foreign selling in the South Korean stock market accelerates, with cumulative net sales reportedly reaching $75 billion this year

On June 9, The Kobeissi Letter, citing Goldman Sachs data, reported that global investors are selling South Korean stocks at an unusually rapid pace. In the latest trading session, foreign investors sold about $801 million worth of Kospi constituent stocks again; total foreign outflows last week reached about $10 billion, and the market has been in net foreign selling on nearly every trading day over the past month. According to the data cited in the report, foreign investors have sold about $75 billion worth of South Korean stocks so far this year. Meanwhile, South Korean retail and institutional investors together recorded roughly $69 billion in net buying over the same period, suggesting that the market’s main buying support has come from domestic capital rather than returning overseas funds. The information currently disclosed still mainly comes from The Kobeissi Letter’s retelling and Goldman Sachs data summaries, while public details on the statistical period and the specific definition of “selling” remain relatively limited.

Fortune Warns of Strategy’s Financing Structure Risks as Bitcoin Premium Narrows

Fortune warned that Strategy’s Bitcoin treasury model faces growing financing risks as MSTR’s net asset premium narrows and preferred stock dividend pressure increases.

Ferrari Challenge Le Mans: Carl Moon to Dominate in WEEX Livery

Sahara AI Responds to SAHARA’s Sharp Drop: No Contract or Product Security Issues Found, Internal Investigation Underway

Sahara AI responded to SAHARA’s 60% price drop, saying no token contract or product security issues have been found and an internal investigation is underway.

WEEX Deposit/Withdrawal Dynamic Island: Your Asset Status, Always in Sight

Scaling Crypto Derivatives: The Digital Asset Infrastructure Behind High-Volume Trading

In the fast-moving digital asset ecosystem, derivatives platforms face an extreme architectural test. High-leverage futures markets demand more than just standard security—they require absolute operational precision, zero-latency matching engines, and ironclad structural scalability, all while navigating intense market volatility.

As global platforms scale to meet these demands, the industry is shifting away from rigid, monolithic setups toward a more agile, "decoupled" infrastructure philosophy.

The Blueprint for High-Volume Copy TradingFor elite global exchanges like WEEX (founded in 2018), this architectural choice becomes critical when scaling high-volume retail features like social copy trading. When thousands of users automatically mirror the real-time strategies of elite traders simultaneously, it triggers sudden, monumental spikes in concurrent transactional volume.

To prevent execution latency or settlement bottlenecks during these peak volatility events, a platform's primary engine must remain entirely dedicated to risk management, copy-trade synchronization, and order matching.

The Architectural Rule: New-generation platforms must separate front-end user execution engines from heavy backend infrastructural overhead to eliminate operational friction.

By separating these layers, platforms can maintain complete sovereignty over their trading environments and user experiences while strategically aligning with institutional-grade infrastructure ecosystems. This strategic framework allows modern exchanges to leverage advanced Digital Asset Custody infrastructure such as Cobo’s behind the scenes, ensuring that backend wallet management scales elastically alongside trading spikes.

Capitalizing on Market Momentum and 400× LeverageIn a derivatives arena where platforms offer up to 400× leverage on perpetual contracts, capital efficiency and market agility are core business metrics. To capture market momentum, an exchange needs the ability to rapidly expand its asset offerings, supporting everything from legacy crypto assets to sudden, trending altcoins across a massive library of trading pairs.

Adopting a flexible, scalable Wallet-as-a-Service (WaaS) solution such as Cobo’s could completely rewrite the development timeline for high-growth exchanges. Instead of spending months of engineering capital building out custom backend wallet architectures for every new blockchain network, platforms can deploy localized infrastructure in days.

This agility allows platforms to instantly scale their listings to over a thousand trading pairs without compromising security or delaying time-to-market. It mirrors the exact operational advantages seen during high-velocity market events, similar to how advanced wallet infrastructure empowers platforms during sudden asset surges; allowing exchanges to pass that speed and liquidity directly to their global user base.

A Mature Foundation for GrowthThe synergy between trusted infrastructure ecosystems and global trading platforms represents the natural evolution of a maturing crypto market. As WEEX continues to scale its global spot and derivatives offerings for over 6 million users, adopting robust backend paradigms proves that platforms no longer have to compromise between cutting-edge trading velocity and uncompromised structural security.

Morning Report | BitMine increased its holdings by 126,971 ETH last week; trader Eugene announced his exit from the crypto market

Wang Chuan: How can one not feel anxious after the neighbor Old Wang made thirty times profit by investing in storage stocks? (Seven) - A quarter-century cycle

Get Paid to Onboard? Try WEEX’s New Homepage with Rewards for Registration, Deposit & Trade

WEEX Custom Layout: Build Your Perfect Trading Workspace in Seconds

See “Buy Walls” & “Sell Walls” Instantly: WEEX Launches the Depth Chart for Smarter Trades

What Is Quick Trade on WEEX? 2 Ways WEEX Ends Chart-Panel Jumping

Morning News | Five major virtual asset platforms in South Korea have experienced 57 incidents of hacking and system failures in six years; Grayscale submits registration application for Canton ETF

$75 billion in foreign capital has fled, and South Korean retail investors have absorbed it all using leverage

Bitcoin Trading Guide 2026: Strategies for Experienced Traders

What Is XAUT and PAXG? Why Tokenized Gold Is Booming in 2026

Cryptocurrency CEXs are flocking to sell US stocks, and traditional brokerages are facing an "uninvited guest."

Will the SpaceX IPO Hurt Bitcoin? Here's What Traders Are Watching

Foreign selling in the South Korean stock market accelerates, with cumulative net sales reportedly reaching $75 billion this year

On June 9, The Kobeissi Letter, citing Goldman Sachs data, reported that global investors are selling South Korean stocks at an unusually rapid pace. In the latest trading session, foreign investors sold about $801 million worth of Kospi constituent stocks again; total foreign outflows last week reached about $10 billion, and the market has been in net foreign selling on nearly every trading day over the past month. According to the data cited in the report, foreign investors have sold about $75 billion worth of South Korean stocks so far this year. Meanwhile, South Korean retail and institutional investors together recorded roughly $69 billion in net buying over the same period, suggesting that the market’s main buying support has come from domestic capital rather than returning overseas funds. The information currently disclosed still mainly comes from The Kobeissi Letter’s retelling and Goldman Sachs data summaries, while public details on the statistical period and the specific definition of “selling” remain relatively limited.